Climate change presents a major challenge for countries, communities,

companies and citizens. According to the

United Nations Framework Convention

on Climate Change

, “Climate change" means a change of climate which is attributed

directly or indirectly to human activity that alters the composition of the global

atmosphere and which is in addition to natural climate variability observed over

comparable time periods. Including anything from shifting weather patterns that

threaten food production, to rising sea levels that increase the risk of catastrophic

flooding, the impacts of climate change are global in scope and unprecedented in

scale. Without drastic action today, adapting to these impacts in the future will

be more difficult and costly.

Climate change is a business risk

Climate change is a business risk. Climate risks will have major implications for most

sectors of our economies. They impact revenues, cash flows and operating costs, asset

values and financing cost, and ultimately the competitiveness and profitability of

firms and financial institutions. The physical effects of climate risk tend to

materially impact industries with physical assets in risk-prone areas (e.g., real

estate in coastal areas or wildfire-prone areas);

industries where infrastructure

resiliency and business continuity are societal necessities

(e.g., health care delivery,

telecommunications / Internet, utilities); and industries dependent on natural capital

(e.g., those that rely on productive land and availability of water, such as agriculture,

meat, poultry, and dairy).Given that businesses face these risks, rational self-interest

of businesses should be a major driver of adaptation actions.

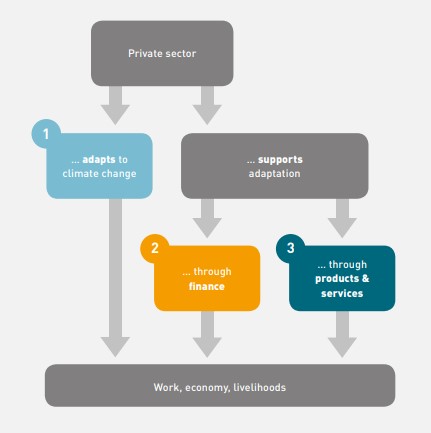

a) The private sector adapts to climate change

Climate change poses a threat not only to individuals, households, and the public sector, but also to the private sector,

both in developed and in developing countries. Slow onset climate change (e.g. temperature increase and sea level rise)

and extreme weather events (such as increasingly intense and frequent storms or heat waves) can:

• directly affect companies, e.g. by damaging their buildings, disturbing production processes and reducing the

productivity of their employees; and

• indirectly affect companies, e.g. if critical transport infrastructure is destroyed, a government issues a new

regulation to reduce vulnerability of its citizens, or if (financial) markets change.

It is important that private entities adapt to climate change simply to ensure their survival. Adapting operations

and business models to climate change can also be an opportunity for companies – it can make them more resilient

to shocks than their competitors and allow them to tap new markets for adaptation products and services. Hence,

adaptation is also a driver of business growth.

In addition, private sector adaptation also has wider effects for societies and economies.

The private sector is

a key contributor

to job creation, economic growth and poverty reduction. In some countries, more than 80 percent

of critical infrastructures (e.g. energy, water, transport, food supply, etc.) are delivered by private actors.

By investing in its own adaptation, the private sector can increase resilience of its stakeholders,

including employees, clients, surrounding communities and local governments.

b) The private sector finances climate change adaptation of others

Private financial institutions and investors

such as banks, pension funds, insurance companies or impact investors can invest in climate

resilience or provide funding for climate change adaptation of others, e.g. through (micro) loans, bonds or venture capital.

Increasing awareness and disclosure of the risks of climate change already today incentivizes financial institutions to shift investments

away from companies and activities, which are vulnerable to the physical, transitional and liability risks of climate change,

towards those that have a sound business case under changing climatic conditions.

While conceptual and practical issues make it difficult to track how much the private sector already invests in adaptation today,

it is clear that significantly more finance from the private sector is needed in order to meet the financing needs for climate change adaptation

c) Private entities support others through products and services for climate resilience

Besides critical infrastructure, jobs and financing, private entities can develop and provide specific products or services that help others become

more resilient and cope with the risks of climate change. For example, in agricultural value chains this may include providing micro

irrigation and heat-resistant crop species to small-scale farmers.

Table 3 proposes potential different roles of different actors and summarizes which of the three roles each type of

company/private player could focus on in order to lever its strength for resilience building.

Gender Action Plan and UNFCCC

A first-ever Gender Action Plan to support gender-responsive climate action is the first UNFCCC Gender Action Plan (COP23, 2017),

which aims to integrate gender equality principle around climate change (nationally and internationally) through five priority areas.

Enhanced Lima Work Programme on Gender (LWPG) (COP 25, 2019)

The Enhanced Lima Work Programme on Gender (LWPG) (COP 25, 2019) and the Gender Action Plan (GAP) set five priority areas to advance the development

of gender-responsive climate actions, which will lead towards increased effectiveness, fairness and sustainability of climate policy and action.

The enhanced five-year GAP is focused on implementation of gender-related activities and affirms that action by all stakeholders

- public and private - towards gender-responsiveness is critical.

TOOLKIT FOR PRIVATE SECTOR ENGAGEMENT IN CLIMATE ACTION

INFO SHEET NO. 1

CLIMATE CHANGE – WHY IT IS RELEVANT FOR THE PRIVATE SECTOR

1.1 What is the climate change expected impact for the Republic of Serbia?

The European climate law is based on Regulation (EU) 2018/1999, which with certain changes became binding for Serbia through the Energy Community Treaty (hereinafter: EnCT), i.e. through the Decision of the Ministerial Council from November 2021 (Decision - Ministerial Council Decision 2021/14/MC-EnC of 30 November 2021 on incorporating Regulation (EU) 2018/1999 in the Energy Community acquis communautaire and amending Annex I of the Treaty).

With this Decision, the member states, including Serbia, undertake to draw up long-term strategies, integrated plans for energy and climate (Integrated National Energy and Climate Plans - NECPs) and reports on the progress or implementation of the NECP, as well as a strategic plan for reducing methane emissions, but also reports on policies and measures to reduce GHG emissions, on GHG projections and on funds collected through carbon taxes or similar mechanisms, as well as strategies and plans for adaptation to changed climate conditions.

The implementation of the aforementioned Decision, as well as visible and ambitious climate actions, in addition to being necessary in order for the Serbian economy to be competitive on the EU and international markets and to protect itself from damages and losses due to climate change, also represent the fulfilment of obligations from the Sofia Declaration (Green Agenda for Western Balkans) and accompanying documents.

Characteristics of climate change

According to official data from the Republic Hydrometeorological Institute (RHMZ), 2019 is the warmest recorded year in Serbia since 1951, and in Belgrade since 1888. Nine of the ten warmest years in Serbia were registered after 2000 (period 1951-2020), and fourteen out of fifteen in Belgrade.

Analysis of climate changes and observed and/or expected climate changes in the Republic of Serbia show that the average temperature in the period 2001-2020. increased by +1.4°C compared to the values in the period 1961-1990. With a maximum increase in the summer season (from +2.2°C). In the period 2021-2040 the expected increase is +2.2°C, which increases to +2.5 to +3.1°C in the period 2041-2060 and goes from +3.1°C to +5.8°C in 2081-2100 compared to 1961-1990.

Increased climate variability means more frequent occurrence of years with drier conditions as well as the aforementioned increase in droughts. A significant impact on drier conditions is the increase in temperature, as well as changes in the precipitation regime. The percentage of years with drought increased by + 30% in 2001-2020 compared to 1961-1990. It is expected that in 2041-2060 every year will be with drought. The frequency of years with severe drought (happened once in 2011-2020) is increasing, in 2021-2040 there will be 2-3 per decade (in a period of 10 years), in 2041-2060 3-4 per decade, and in 2081-2100 can be expected in 7-8 years per decade. Thus, one can expect an extension of the period of low flows in the rivers, a decrease in the rate of groundwater renewal and a decrease in the average soil moisture.

What is of additional concern is the observed and expected increase in the number of occurrences of heat waves per year (in the period 1961-1990 there were less than 1, and in the period 2001-2020. even +2.4, of which +3 in the period 2011-2020) , days with high temperatures (maximum daily over 30°C and over 35°C), days with very heavy (daily precipitation 20mm-30mm) and extreme (daily precipitation over 30mm) precipitation (which result in an increase in the risk of floods and erosion )

Analysis of the impact of climate change have shown that the sectors of agriculture, water resources management and forestry are most affected, as well as energy and infrastructure, which result in additional impacts on health and the healthcare system of the Republic of Serbia.

Threats and risks due to climate change

In addition to the obligations arising from international agreements and EU legislation, Serbia has the obligation to plan and implement measures and activities to adapt to changed climate conditions, due to increasing damages and losses caused as a result of climate change. The results of analyzes and modeling show that the increase in the average global temperature can have a significant impact on the total value of the GDP of the Republic of Serbia in the absence of adaptation/adjustment to the changed climatic conditions. The reduction of the total GDP in relation to the potential that would have been achieved without global warming and without adaptation to changed climate conditions is shown in Table 1. Additionally, it should be borne in mind that in 2030 a loss of 0.03% of working hours can be expected that is, a thousand jobs just because of heat waves, mostly in the agriculture and construction sectors.

Temperature increase:

2020-2040

2040-2100

2020-2100

1°C

15,465 (1,20%)

328,899 (4,74%)

344,364 (4,19%)

2°C

58,124 (4,53%)

708,193 (10,2%)

766,317 (9,32%)

3°C

59,107 (4,97%)

831,296 (12,88%)

890,403 (11,65%)

4°C

97,536 (6,87%)

1.904,874 (18,46%)

2.002,41 (17,06%)

According to estimates from the first NDC, Serbia in the period 2000-2015. suffered damages of over 5 billion euros due to natural calamities and natural disasters, more precisely caused primarily by droughts (over 3.5 billion euros), floods (over 1.5 billion euros) and forest fires (about 300 million euros in the period 2000-2009 ). The need for investment in adaptation is also confirmed by the assessment of minimum damages and losses of 7 billion USD in the period 2000-2020. years, caused by natural disasters and natural disasters. Most of which is the result of droughts and high temperatures. On the other hand, only the flood in 2014 showed sensitivity to natural disasters, resulting in a total damage of EUR 1.7 billion or more than 4% of GDP. In addition, it should be borne in mind that more than 18% of Serbia's territory is exposed to floods and torrential floods, 21% of the territory is exposed to droughts, and the risk of forest fires is present on 3.6% of the territory and increases from year to year.

Climate risks for private sector can be divided into

Direct and indirect risks :

xIncreasing water scarcity and changes in the availability of natural resources

xPhysical impacts of extreme weather events and sea-level rise on utilities and infrastructure

xChanging demand for consumer and intermediary goods and services

xHealth issues affecting workers and consumers (e.g., heat waves or infectious diseases)

xRegulatory uncertainty as governments prepare to cope with climate impacts (e.g., new water regulations and changes to zoning laws due to expanding flood zones)

xReputational consequences for companies that are seen as failing to support their communities

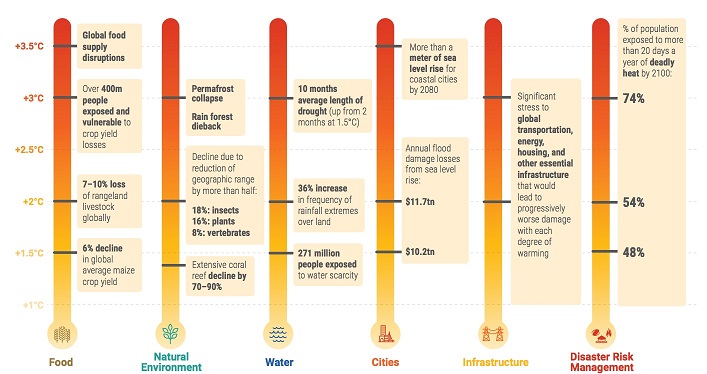

Figure 1 Risks of catastrophic events increases with temperature

(Adopted from World Resource Institute and CCA report 2019)

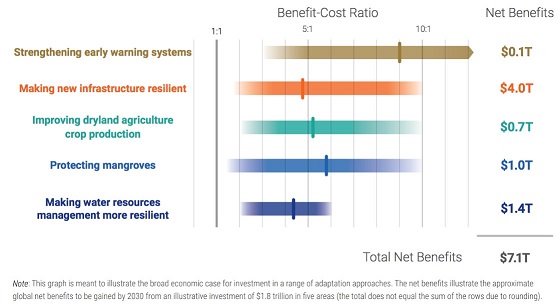

Figure 2 Benefit cost ratio of climate investment in adaptation

Accelerated investment in climate change resilience is urgently needed to ensure the

well-being of economies, companies and people. According to the Global Commission on adaptation report

published in 2019, investing $1.8 trillion globally in five areas: strengthening early warning systems,

making new infrastructure resilient, improving dryland agriculture crop production, protecting mangroves

and making water resources management more resilient from 2020 to 2030 could generate $7.1 trillion in

total net benefits. Thus, the overall rate of return on investments in improved resilience is very high,

with benefit-cost ratios ranging from 2:1 to 10:1, and in some cases even higher (Figure 2).

Global response to the climate challenge

The United Nations Framework Convention on Climate Change (UNFCCC) entered into force on 21 March 1994.

Today, it has near-universal membership. The 197 countries that have ratified the Convention are called

Parties to the Convention. Preventing “dangerous” human interference with the climate system is the

ultimate aim of the UNFCCC.

The Paris Agreement is a legally binding international treaty on climate change. It was adopted by 196

Parties at COP 21 in Paris, on 12 December 2015 and entered into force on 4 November 2016. Its goal is

to limit global warming to well below 2, preferably to 1.5 degrees Celsius, compared to pre-industrial

levels. To achieve this long-term temperature goal, countries aim to reach global peaking of greenhouse

gas emissions as soon as possible to achieve a climate neutral world by mid-century. The Paris Agreement

is a landmark in the multilateral climate change process because, for the first time, a binding agreement

brings all nations into a common cause to undertake ambitious efforts to combat climate change and adapt

to its effects.

Implementation of the Paris Agreement requires economic and social transformation, based on the best available

science. The Paris Agreement works on a five-year cycle of increasingly ambitious climate action carried out

by countries. By 2020, countries submit their plans for climate action known as Nationally Determined Contributions (NDCs).

International agreements, such as the

2030 Agenda for Sustainable Development, the Addis Ababa Action Agenda and

the Paris Agreement

on climate change all strongly emphasise the critical role for the private sector in achieving

development outcomes, both as a source of finance as well as know-how. There is also clear recognition across the

development co-operation community of the central position private sector actors can play in supporting the

implementation of Nationally Determined Contributions (NDCs) – as drivers of green growth in developing countries,

promoters of green supply chains, as a source of investment in low-carbon, climate-resilient infrastructure,

and as leaders in innovation in clean technologies and resource efficiency. In recognition of this, the OECD

Development Assistance Committee is looking at the lessons learned and best practice experiences from efforts

to engage the private sector for development outcomes, more broadly, and in relation to green growth and

climate change, in particular.

Nationally Determined Contributions (NDCs) are the expressions of efforts made by countries in

reducing national emissions and adapting to the impact of climate change. NDCs are at the heart

of the Paris Agreement and the achievement of these long-term goals. The Paris Agreement requires

each party to outline and communicate the NDCs that it intends to achieve. The UNFCCC receives

and records NDCs in a public registry.

National Adaptation Plans (NAPs) are plans made to identify a country's medium- and long-term climate

adaptation needs, as well as strategies and programmes that need to be developed and implemented to

address those needs. The development of NAPs is a continuous, progressive and iterative process,

following a country-driven, participatory and transparent approach. These planning processes are

intended to catalyse action and finance to generate systemic change that addresses climate impacts and

vulnerabilities. Taking effective climate action requires countries to work out what kinds of adaptation

measures will be effective. That is why the proper planning and formulation of National Adaptation Plans

(NAPs) and/or other planning processes are so important.

Climate Change Adaptation and Mitigation

Adaptation refers to adjustments in ecological, social, or economic systems in response

to actual or expected climatic stimuli and their effects or impacts. It refers to changes

in processes, practices, and structures to moderate potential damages or to benefit from

opportunities associated with climate change. In simple terms, countries and communities

need to develop adaptation solution and implement action to respond to the impacts of

climate change that are already happening, as well as prepare for future impacts. (UNFCCC)

As there is a direct relation between global average temperatures and the concentration

of greenhouse gases in the atmosphere, the key for the solution to the climate change

problem rests in decreasing the amount of emissions released into the atmosphere and in

reducing the current concentration of carbon dioxide (CO2) by enhancing sinks

(e.g. increasing the area of forests). Efforts to reduce emissions and enhance sinks are

referred to as “mitigation”. (UNFCCC)

The difference between climate change mitigation and climate change adaptation is that mitigation is

aimed at tackling the causes and minimising the possible impacts of climate change, whereas adaptation

looks at how to reduce the negative effects it has and how to take advantage of any opportunities that

arise. Where mitigation strategies fail to reach emissions containment targets, climate resilience will

be key to lessen the impacts of climate change and pave the way for as more sustainable and environmentally

sound development.

How can private sector participate/contribute to strengthening climate governance? Global perspective

There is no single blueprint of private sector engagement

in climate governance and climate action, and the engagement of private sector is country and region specific. Yet, some of the approaches for state-business

partnerships for sustainable development can include:

ensuring additionality of private sector efforts (i.e. going beyond what business would have invested in anyway); financial sustainability of approaches; mutual transformation (i.e. changing of attitudes and business models); and risk-sharing,

all within a transparent manner without market distortion

(Garside et al (2016).

Over the course of Green Climate Fund (GCF) engagement in various countries, a couple of roles of private sector potential engagement have been identified, including:

Private sector actors who make direct investments—whether in the form of debt or equity—in projects.

These actors include institutional investors (including sovereign wealth funds, endowments, pension

funds, mutual funds, insurance companies, hedge funds, and private equity firms), commercial banks,

and corporations making internal capital allocation decisions. Some capital providers may also act as

project developers or market facilitators.

Around the world, companies are putting in place measures to anticipate for and adapt to climate impacts,

otherwise known as ‘’adaptation’’. Companies recognize that their ability to grow and prosper cannot be disconnected

from community well-being. Companies view building community climate resilience as an imperative for strategic business

action that must go beyond the realm of corporate philanthropy.

by companies at COP 21 include the Science Based Targets initiative, which saw 144 companies commit to set targets in line with the overarching

2C temperature goal of the Paris Agreement, and the Paris Pledge for Action or ‘L’Appel de Paris’, which united 400 businesses

and 120 investors with other non-state actors in committing to support the delivery of the Paris Agreement (Science Based Targets,

n.d.; COP 21, 2015). The Global Commission on Business and Sustainable Development, headed by Unilever, highlights why companies

need to engage in delivering the SDGs: economic benefits from new markets and innovation, risks to business performance and stability,

and the necessity to work closer with the government and other stakeholders in the future (Business and Sustainable Development Commission, n.d.).

is an investor initiative to ensure the world’s largest corporate greenhouse gas emitters take necessary action on climate change.

The companies include 100 ‘systemically important emitters’, accounting for two-thirds of annual global industrial emissions,

alongside more than 60 others with significant opportunity to drive the clean energy transition. Launched in December 2017 at the

One Planet Summit, Climate Action 100+ garnered worldwide attention as it was highlighted as one of 12 key global initiatives to tackle climate change.

Private sector actors who provide critical financial services. Examples include insurance companies

(who offer products that can reduce project and market risks), financial institutions (who provide

underwriting, advisory, and other financial services), liquidity providers (who provide short- term

loans and/or currency exchange services), rating agencies (who evaluate a project's ability to repay

its debt), and data providers (providing market information). “Market Facilitators” are critical to

market creation and growth.

Entities (ranging from small and medium enterprises to larger corporations) undertaking projects and seeking

financing. Project developers often act as “Capital Providers” since they typically provide a portion of a

project's financing through their own capital contribution (also known as an “equity stake”). In the case

of low-carbon development, projects can range from wind and solar installations, to energy efficiency

retrofits, to biomass and waste-to- energy conversion facilities.

To understand the current and potential

contribution of the private sector to the delivery of the climate agenda, it is important to highlight what we mean by ‘private sector’ .

The term ‘private sector’ refers to a broad range of individual professionals and companies interacting with each other within diverse

associations, public-private partnerships and the community, such as:

• Investors, land- and business- owners. These include individuals and companies, private financial institutions,

pension funds, as well as public estate companies acting as private bodies and blurring the line between ‘public’ and ‘private’;

• Developers and contractors;

• Architects, engineers, landscape and urban design/planning practitioners;

• Consultants to the public or private actors involved in research and development and capacity building (knowledge providers);

• Service managers facilitating interaction between local authorities and private contractors/ communities;

• Service providers, for example, transport, energy, and waste companies.

• Businesses involved in the production of climate technology, hereunder-renewable energies, such as windmills, solar cells, etc.

2.2 Climate risks for the private sector

Today it is generally accepted that climate risks are also common

risks that trigger private sector investments. The potential impacts of climate change on the private sector is not only physical and do not only manifest in the

long term. Climate related risks are created by a range of weather hazards. Some are slow in their onset (such as changes in temperature and precipitation leading

to droughts, or agricultural losses), while others happen more suddenly (such as tropical storms and floods). There is scientific evidence for the expected climate

impacts, but uncertainty regarding the magnitude of the impacts, such as due to increasing temperature and sea level rise is expected.

The profile of private sector actors operating under the “risk-return” scheme and subject to climate risks may change significantly, since such organizations may be

more susceptible to the physical effects of climate change, climate policy and new technologies. These climate risks include:

2.3 What is the role of private sector in addressing climate change?

Generally, the private sector has an important role in delivering climate goals,

typically based on a partnership or collaborative approach involving all sectors and emphasizing the role of cities, public agencies, and civil society. There is a growing reliance

on the private sector’s contributing role, suggesting that governments cannot singularly manage development and drawing attention to benefits related to private-sector involvement in development.

Clearly, involving the private sector can help in terms of capacities as no local or national government can mobilize necessary capital

and political consensus to make effective investments in infrastructures leading to sustainability. There is an ‘unrecognized opportunity for the private sector to engage in selective

investments that can help cities limit the effects of these trends (meeting the need of urbanizations and shortage of resources, energy, clean air)’. A related idea is that private

parties can be incentivized to mobilize their capacities, so they can deliver verifiable climate outcomes and make a material contribution to closing the emissions gap’. At the same

time, these contributions would be broad ranged. Emissions-reduction and adaptation projects also deliver other benefits than climate adaptation and mitigation, such as health

improvements and biodiversity conservation, and can be part of more holistic plans contributing to social, environmental, and economic benefits.

Private sector can engage with various climate adaptation activities to reduce climate related risks to core business operations,

and in climate mitigation activities to promote green and efficient development. These actions not only reduce risks for private sector entities, but also contribute to national

and global efforts to address climate change. ;

Private actors involved in sustainability practice, whether occupying a space, involved in industrial production, in construction or

service delivery (water, waste) ought to be committed to reducing CO₂ emissions through internal and external processes in compliance with national and local regulations.

They should be committed to designing products and processes to limit CO₂ emissions.

It should be noted that the degree of private sector involvement in climate finance directly depends on the level of development of the sector and is largely determined

by the national development context of countries.

2.3.1 Reducing climate related risks to private sector core business operations (adaptation)

According to the Global Commission on Adaptation (GCA) report, without adaptation to climate change, the following losses are envisioned globally:

• Depressed growth in global agriculture yields up to 30% by 2050. About 500 million small farms around the world will be most affected.

• The number of people who may lack sufficient water, at least one month per year, will soar from 3.6 billion today to more than 5 billion by 2050.;

• Rising seas and greater storm surges could force hundreds of millions of people in coastal cities away from their homes, with a total cost to coastal urban areas of more than $1 trillion each year by 2050.

• Climate change could push more than 100 million people within developing countries below the poverty line by 2030.

Thus, the GCA initiative proposes a triple dividend approach to private sector adaptation to climate change: avoiding losses, economic benefits and social and environmental benefits:

Yields for private sector of investing in climate change adaptation

Challenges and opportunities for adaptation (GCA examples)

50 percent increase in global demand for food between 2010 and 2050

R&D investment is crucial to address climate stresses on crops from increasing heat, drought, and disease.

In Zimbabwe, farmers using drought-tolerant maize were able to harvest up to 600 kilograms more maize per

hectare than farmers using conventional maize.

70% increase of demand for meat, dairy, and fish by people in developing countries.

Private finance models that works for small-scale producers and cooperatives, including microfinance.

Investments in basic and applied research in both national

and internationally oriented research agencies as well as extension services have high rates of return.

Depressed growth in global yields by 5–30 percent by 2050.

Equal property rights for women to advance gender justice for female farmers.

Increased variability and extremes in temperature and rainfall will lead to production shocks that will worsen food insecurity.

Development of new marketing and export networks.

Increased food prices (by 20%), reduce food availability, and reduce the incomes and food production of smallholder farmers.

Exploit digital technology, better weather information, and farmer to-farmer education.

Challenges/Opportunities

Actions

Examples

Lack of private sector investment in nature-based solutions

Public private partnerships with national and local governments to reorient policies,

subsidies and investments, including developing programs to better mobilize private sector support

Examples include payments for ecosystem services (PES), green bonds, resilience bonds, insurance schemes, and water user fees.

Challenges/Opportunities

Actions

Examples

Crucial water supplies, like aquifers and lakes, are shrinking or increasingly polluted.

Floods and droughts cause damages

in the billions of dollars and take a huge human toll, in particular on women and girls

Irrigation modernization, including using new techniques such as just-in-time irrigation,

coupled with climate-appropriate agricultural policies, can slash the amount of water needed

in agriculture, which now accounts for about 70 percent of global water use. This can be done while also increasing yields.

In response to poor water supplies, system leaks and financial mismanagement of utilities

in Karnataka,

India, a water use efficiency scheme was developed

, with reduction of leakages as a main climate adaptation

strategy. With public-private partnership (PPP) contracting planning support from

Public Private Infrastructure

Advisory Facility (PPIAF)

, a pioneering design, build, operate (DBO) contract for privately operated water service

in the North Karnataka cities of Hubballi Dharwad, Belgaum, and Kalaburagi was implemented. Service and availability

of water jumped from 10 hours a week to 24 hours a day. To boot, the volume of water lost to leakages was reduced

by 2 500 m3/day proving that 24/7 water service was possible in India while improving water resource resilience to droughts.

Challenges/Opportunities

Actions

Examples

While spreading and growing, many cities have been relentlessly stripping away or building over floodplains,

forests, and wetlands that could have absorbed stormwater or offered respite and precious water

during heat waves and droughts.

Knowledge providers to make the latest modeling technologies and credible data on climate risks

available to cities and communities.

Need for updated topographic maps, along with weather and climate information, satellite, and remote

sensing data; models that reveal risks of climate impacts to local areas; and assessments of the

vulnerabilities for specific population groups, such as women and people living in poverty

City governments and private actors to build capacity to use this information in order to drive

integrated urban planning, investments, and operations and reduce climate risks.

International financial institutions, donors, and the private sector to step up finance for urban adaptation,

and to prioritize valuing and incentivizing such investments.

2.3.2 How exactly can the private sector contribute to climate change adaptation?

Implementing adaptation measures to protect own assets and operations

Tire manufacturer improves water efficiency of production process

Several food stall owners jointly invest in installation of sun blinds to protect themselves from direct sunlight

Small-scale, local private entities have to focus, first and foremost, on protecting their immediate operations

and assets. Given low financial resources, financing climate change adaptation of others does not seem to be a

priority for these actors. Yet, considering how difficult it is for many of the smaller, informal companies,

to access funding from financial institutions (IFC 2010), their role in financing each other’s adaptation through

peer-to-peer lending might have to be reconsidered.

Adaptation products and services can open up new opportunities for those who have the resources and flexibility

to adapt their business models accordingly.

Provide finance

Providing small-scale financing for business partners

Roaster pays in advance to allow coffee farmer to purchase irrigation equipment

Offer products & services

Offer products & services Offering products or services that can help clients adapt to climate change

Gardening company builds green spaces in urban heat trapped areas.

Individual business development consultant integrates resilience into advisory for agricultural processing companies.

Large enterprises and multinational corporations

Activities

Examples

Possible focus of adaptation efforts

Adapt to climate change

Implementing adaptation measures to protect own assets and operations

Car manufacturer improves storm resistance of headquarter offices.

Large and multinational companies need to make their own operations and assets resilient

but should also support their suppliers and business partners – financially and through

other inputs, e. g. organizational help for local adaptation – in order to avoid business

interruption. Adaptation can potentially be a large business opportunity for companies that

already have clients, which are increasingly vulnerable or want to access new markets

(see, for example, UN Global Compact and UNEP 2012).

Provide finance

Providing finance for adaptation of companies in the value chain

Food company pays higher per-unit price to finance adaptation of small-scale farmers who supply raw goods

Offer products & services

Otherwise supporting adaptation of suppliers or business partners

Textile company helps organize local adaptation round tables with companies and government .

Offer products & services

Offering products or services that can help clients adapt to climate change

Solar panel manufacturer sells solar panels to improve access to energy

Large rating agency develops rating methodology for adaptation bonds

[1] Annica Cochu, Tobias Hausotter., Mikael Henzler., The Roles of The Private Sector In Climate Change Adaptation – An Introduction, adelphi research gemeinnützige GmbH, July 2019, p. 5-6

2.3.3 Promoting green and efficient private sector development (mitigation)

As public finances become increasingly constrained, there is a clear need to find resources from elsewhere to support the move

to a low carbon, resilient society with private sector engagement. Clearly, the private sector has an important role to play

in building a low-carbon, climate resilient future for the planet.

Some companies are already hard at work developing weather-based insurance products that provide financial payouts to farmers

in the event of a drought or a flood, for example, allowing farmers to hedge against the risks that are becoming more acute

due to the impacts of climate change. Other companies are co-financing infrastructure projects, while others are making

their own supply chains and business operations more climate resilient.

New international and national policies aim at encouraging these private actors. Examples include the UN Framework

Convention on Climate Change, which has a Private Sector Initiative to catalyse the role of the private sector

in climate adaptation, and forms of climate finance, such as the Climate Investment Funds, which place a special

emphasis on involving the private sector in climate resilience

However, the private sector has generally focused on climate mitigation by, for example, reducing emissions through

developing renewable energy and energy efficient technologies. Financing adaptation has been less of a strong

point and risks being left out. For example, solar lanterns may be sold to communities without access to electricity

by private companies. The lanterns are low carbon (as they are a renewable source of energy) and can increase the

resilience of families to the impacts of climate change by offering them a cheaper and reliable source of light,

and don’t create the health problems caused by burning wood or charcoal, which is a major cause of disease. This

allows families to save money, stay healthy and allows children to study and do better at school. All of these

factors will make a family more climate resilient and so recover more quickly to any unexpected shocks, such as a flood or a drought.

2.3.4 Main barriers for further private sector investment towards climate change action

The main barriers to for companies to invest in climate-related technologies are:

- the lack of clarity regarding domestic regulations

- lack of understanding of climate finance

- lack of access to timely information, lack of understanding of climate technologies and lack of qualified staff

- lack of R&D / technical assistance; lack of own funds; lack of funds in the market; lack of clarity regarding EU regulations; and lack of innovative ideas

To encourage investments in climate-related technologies, the following main drivers are suggested through consultations with the Serbian private sector:

• Simpler procedures (19 percent of respondents)

• Tax incentives / tax breaks (19 percent of respondents)

• Clearer guidance by state institutions (technical experts, feasibility studies) (16 percent of respondents)

• Availability of State aid (12 percent of respondents) and lack of innovative ideas

• Interest rate and grace period of loans (7 percent of respondents)

• Guidance by development banks on types of financial products/instruments (6 percent of respondents)

• Networking with government officials (6 percent of respondents)

• Export facilitation (6 percent of respondents)

• Improving company reputation (4 percent of respondents)

• Market exposure (4 percent of respondents)

• Guidance by private banks on types of financial products (1.4 percent of respondents)

Capacity issues were also uncovered by the same consultation process. Respondents indicated that they would need help with:

• Undertaking feasibility studies

• Project preparation and administration

• Training in emerging technologies or processes relevant to the green economy

• Reporting on environmental performance indicators

• Financial forecasts

• Training in financing arrangements with banks

The following topics were identified as training and capacity-building needs:

• Climate finance – what it entails, main actors and how to access?

• Basics of climate change adaptation strategies and climate change mitigation strategies

• Basic and advanced courses on Sustainable Development Goals and Agenda 2030 - linking the goals for sustainable development with climate action

• Understanding which activities already undertaken by companies are related to climate action and climate finance

• Sharing the examples of successful technology transfer projects with the centers abroad

• Development of the in-country expert base for carbon foot-print measurements in collaboration with academia and international organizations

• Development of the capacity building projects for various stakeholders on measuring methodologies

• Capacity building on EU taxonomy and Carbon Border Adjustment Mechanism (CBAM)

• Developing capacity building programs for local financing institutions to support technology transfers.

The priority areas to strengthen the dialogue and partnership between the public and private sectors, as well as increase access to climate finance include:

• Building partnerships between institutions and other sectors in order to maximize efforts, utilize all existing expertise and potential institutional capacity to achieve better results

• Introduction of a portfolio of joint climate and green investments of the private and public sector

• Analysis of existing legislation related to supporting the development of the private sector (example Smart Specialization) in order to incorporate elements to support climate and green investments of the private sector

• Greater understanding on behalf of the government and orientation to taking more interest in the actions that would help businesses respond to requirements of the EU markets

• Identifying in-country sources that are needed in specific sectors and facilitate access and transfer

• Providing access to companies to new, additional funds for climate investment in order to reduce risk and mobilize private green capital

• Creation of a portfolio of public-private partnerships for climate investments, portfolio of private climate investments with the support of state aid

• Creating financial rewards for champions in climate investment

• Supporting private investment funds that invest in climate and green investments of the private sector to reduce financial risks

• Reduction of corporate taxes for companies investing in climate and green investments

Some of the above barriers can (and already are) be(ing) addressed via GCF Readiness support.

Climate finance refers to local, national or

transnational financing—drawn from public, private and alternative sources of financing—that seeks to support mitigation

and adaptation actions that will address climate change.

The Standing Committee on Finance of the UNFCCC

(United Nations Framework Convention on Climate Change - UNFCCC) has proposed activity-based definition of climate finance

that covers both, mitigation and adaptation actions: “Climate finance aims at reducing emissions, and enhancing sinks of

greenhouse gases and aims at reducing vulnerability of, and maintaining and increasing the resilience of,

human and ecological systems to negative climate change impacts”.

The United Nations Framework Convention on Climate Change (UNFCCC) underlines that climate

change is one of the greatest challenges of our time. It emphasizes strong political will

to urgently combat climate change in accordance with the principle of common but differentiated

responsibilities and respective capabilities. To achieve the ultimate objective of the Convention

to stabilize greenhouse gas (GHG) concentration in the atmosphere at a level that would prevent

dangerous anthropogenic interference with the climate system, recognizing the scientific view that

the increase in global temperature should be below 2 degrees Celsius, the Parties shall, on the

basis of equity and in the context of sustainable development, enhance their long-term cooperative

action to combat climate change. They recognize the critical impacts of climate change and the

potential impacts of response measures on countries particularly vulnerable to its adverse effects

and stress the need to establish a comprehensive adaptation programme including international support.

The UNFCCC, the Kyoto Protocol and the Paris Agreement call for financial assistance from parties with more

financial resources to those that are less endowed and more vulnerable. Climate finance is needed for mitigation,

because large-scale investments are required to significantly reduce or sequester GHG emissions. Climate finance

is equally important for adaptation, as significant financial resources are needed to adapt to the adverse effects

and reduce the impacts of a changing climate.

The second Biennial Assessment and Overview of Climate Finance Flows of the UNFCCC, released in November 2016,

recorded USD 41 billion of public international finance flowing to developing countries in 2013-14. In 2018,

the third Biennial Assessment recorded that this had reached USD 56 billion annually in the period 2015-2016

(UNFCCC, 2018). These figures remain relatively small, however, compared to global climate finance estimates,

taking into account all countries and both private and public finance, of USD 579 billion a year in the 2017-2018

period (CPI, 2019).

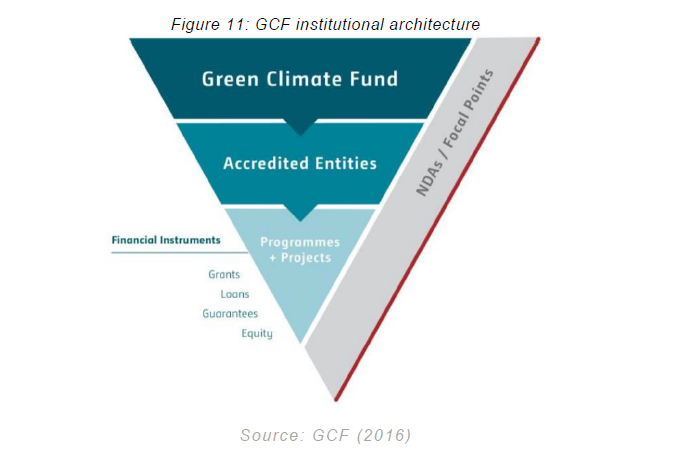

• Accredited Entity. An Accredited Entity is a national, regional or multilateral institution that meets a fund’s standards

and achieves a given accreditation status. It can be private, public or non-governmental entity. Entities can become accredited

as implementing, delivery or executing entities (depending on the funds, see “Implementing Entity” below).

• Additionality. Additionality refers to the use of development funding to achieve climate-related objectives besides regular,

business-as-usual development. Some funds (like the Green Climate Fund (GCF) or the Global Environmental Facility (GEF) Special

Climate Change Fund) will not fund projects that are development projects with a climate change adaptation or mitigation co-benefit.

Instead, the core focus of the project needs to be on climate change, and the fund’s money will be spent in addition to other

development funding. Additionality is an important and politically-sensitive concept that is still being debated on the international stage.

• Annex I Parties. Industrialized countries listed in the United Nations Framework Convention on Climate Change (UNFCCC) Annex I and

committed to reducing their greenhouse gas emissions. Most of these Parties signed the Kyoto Protocol and the Paris Agreement. See the list HERE.

• Annex II Parties Annex II Parties consist of the OECD members of Annex I, but not the EIT Parties. They are required to provide financial

resources to enable developing countries to undertake emissions reduction activities under the Convention and to help them adapt to adverse effects of

climate change. In addition, they have to “take all practicable steps” to promote the development and transfer of environmentally friendly technologies

to Economy in Transition (EIT) Parties and developing countries. Funding provided by Annex II Parties is channeled mostly through the UNFCCC’s financial mechanism.

• Clean Development Mechanism. “Clean Development Mechanism’’ (CDM) is a mechanism under the Kyoto Protocol through which developed countries may finance

projects on reduction or removal of greenhouse gas emissions in developing countries, and, in return, receive carbon credits for doing so which they may apply

to meeting mandatory limits on their own emissions.

• Climate Action Plan. A Climate Action Plan (CAP) is a detailed and strategic framework for measuring, planning, and reducing greenhouse gas (GHG)

emissions and related climatic impacts. Local governments design and utilize climate action plans as customized roadmaps for making informed decisions

and understanding where and how to achieve the largest and most cost-effective emissions reductions that are in alignment with other municipal goals.

Climate action plans, at a minimum, include an inventory of existing emissions, reduction goals or targets, and analyzed and prioritized reduction actions.

Ideally, a climate action plan also includes an implementation strategy that identifies required resources and funding mechanisms.

• Development Finance Institutions. National and international development finance institutions (DFIs) are specialized development banks

or subsidiaries set up to support development projects and programmes in developing countries. They are usually majority-owned by national governments

and source their capital from national or international development funds or benefit from government guarantees. This ensures their creditworthiness,

which enables them to raise large amounts of money on international capital markets and provide financing on very competitive terms.

• Direct Access Entities. A mechanism in which national accredited entities (direct access entities) of developing countries gain direct

access to funding provided by an international fund to implement the selected projects and/or programmes. These entities may wish to choose other

executing entities to carry out the work.

• Financing Mechanism. Developed country Parties shall provide financial resources to assist developing country Parties in

implementing the UNFCCC Convention. To facilitate this, the Convention established a Financial Mechanism to provide funds to developing

country Parties. The operation of the Financial Mechanism is entrusted to the Global Environment Facility (GEF) and the Green Climate

Fund (GCF).

• Implementing Entity. Generally, an “Implementing Entity” (IE) is responsible for vetting and endorsing project and programme

proposals, and for disbursing funding from a fund when proposals are successful. The term IE can vary slightly depending on the Fund.

o The Adaptation Fund accredits national, regional or multilateral IE. The IE works with an Executing Entity, in charge of the day-to-day

management and on-the-ground interventions.

o The equivalent of IE for GEF is called “Implementing Agency” (IA). IAs can be national (e.g. Development Bank of South Africa),

regional (e.g. West African Development Bank) or multilateral (e.g. United Nations Environment Programme). NGOs can also become

accredited as IAs (e.g. World Wildlife Fund). Like with the AF, a GEF Implementing Agency works with an Executing Entity.

o The equivalent of IE for GCF is called “Delivery Partner”. The Delivery Partner may work with an “Executing Entity”.

• Multilateral Development Bank (MDB). Multilateral development banks (MDBs) can be categorized in many ways. The two biggest

groups are “main” and “sub-regional” multilateral development banks:

a) Main: created by a group of countries to provide financing and professional advising for development purposes. For example:

World Bank, the Asian Development Bank, the Inter-American Development Bank Group etc.

b) Sub-regional: for a better deal, banks lend to their members, borrowing from the international capital markets.

Because there is effectively shared responsibility for repayment, the banks can often borrow more cheaply than could any one member nation.

For example: Caribbean Development Bank, West African Development Bank

• National Adaptation Plan (NAP). A process established under the Cancun Adaptation Framework (CAF). It enables Parties to

formulate and implement national adaptation plans (NAPs) as a means of identifying medium- and long-term adaptation needs and

developing and implementing strategies and programmes to address those needs. It is a continuous, progressive and iterative

process which follows a country-driven, gender-sensitive, participatory and fully transparent approach.”

• Nationally Determined Contributions (NDCs). “The Paris Agreement requires each Party to prepare, communicate and maintain

successive nationally determined contributions (NDCs) that it intends to achieve in order to reduce national emissions and adapt

to the impacts of climate change. Parties shall pursue domestic mitigation measures, with the aim of achieving the objectives of

such contributions.”

• Non-Annex I Parties. Non-Annex I Parties are mostly developing countries. Certain groups of developing countries are

recognized by the UNFCCC Convention as being especially vulnerable to the adverse impacts of climate change, including countries

with low-lying coastal areas and those prone to desertification and drought. Others (such as countries that rely heavily on income

from fossil fuel production and commerce) feel more vulnerable to the potential economic impacts of climate change response measures.

The Convention emphasizes activities that promise to answer the special needs and concerns of these vulnerable countries, such as

investment, insurance and technology transfer.

• Official Development Assistance (ODA) refers to financial assistance provided to developing countries and the multilateral

institutions by official agencies, including state and local governments of developed countries for promotion of their economic

development and welfare. In 1970, it was agreed that developed countries would provide 0.7 per cent of their Gross National Income

(GNI) as ODA to developing countries. ODA is also known as foreign aid.”

• Climate finance. The 2016 Biennial Assessment and Overview of Climate Finance Flows (UNFCCC), refers to climate

finance as financial resources dedicated to adapting and mitigating climate change globally, aiming at reducing GFG emissions,

reducing vulnerability, and maintaining and increasing the resilience of human and ecological systems to the negative climate change impacts.

• Climate Public Expenditure and Institutional Review. (CPEIR) is a methodological tool to analyze, how climate change related

expenditure is being integrated into national and sub-national budgetary processes. It has three key pillars: Policy Analysis,

Institutional Analysis and Climate Public Expenditure Analysis. It supports to identify and track climate related expenditure

in the national budget.

• Co-financing refers to conditions that recipient entities need to fulfil to receive financial support from funds.

These conditions may include earmarking funds to certain sectors, co-financing, procurement design, fulfilling certain

criteria under social and environmental context, etc.

• Conditionality refers to conditions that recipient entities need to fulfil to receive financial support

from funds. These conditions may include earmarking funds to certain sectors, co-financing, procurement design, fulfilling certain

criteria under social and environmental context, etc.

• Leverage is used in the context of climate finance in which it refers to public finance (e.g. from international

finance institutions) that is used to encourage private investors to back the same project. This can be in the form of loans,

risk guarantees and insurance or private equity. This is also intended to reduce the perceived risk for the private sector.

Financial institutions apply the terminology ‘leveraging’ to understand how their core contributions (for example, money

provided by donor governments to a multilateral development bank) can be invested in capital markets to create an internal

multiplier effect.

• On-lending. An entity accredited under specialized fiduciary standards can receive money from a fund with

the intention of lending it to other executing entities for the implementation of selected programmes and/or projects.

This can also include providing equity or guarantees to other entities.

• Project Preparation Facility (PPF) is used as means of developing bankable, investment-ready projects.

A PPF may provide both technical and/or financial support to project owners/concessionaires. Such supports can cover a wide range

of activities including: undertaking project feasibility studies including value for money analysis; developing procurement documents

and project concessional agreements; undertaking social and environmental studies; and creating awareness among the stakeholders.

• Technical assistance is non-financial assistance provided by local or international specialists.

It can take the form of sharing information and expertise, instruction, skills training, transmission of working knowledge,

and consulting services and may also involve the transfer of technical data.

3.4 Key climate finance actors and sources

Public finance flows are those carried out by central, state or local governments and their agencies at their own risk and responsibility. Public finance actors include:

• Governments through their ministries, departments and aid agencies.

• Development finance institutions – either national or multilateral; development bank or export-credit agency.

• Climate funds - predominantly multilateral climate funds established under international environmental agreements.

Private finance flows are financial flows at market terms financed out of private sector resources (changes in holdings of private,

long-term assets held by residents of the reporting country) and private grants (grants by non-government organisations,

net of subsidies received from the official sector). Private finance actors include:

• Private companies

• Local, regional and global commercial banks

• Non-bank financial institutions

• Leasing companies

• Private equity investors

• Institutional investors

• Households – family-level economic entities, high net-worth individuals (HNWI),

and their intermediaries (e.g. family offices investing on their behalf).

3.5 Public climate finance

Climate finance globally provided by public sources increased 18% from USD 215 billion annually in 2015/2016 to USD 253 billion in 2017/2018,

and the overall share of tracked climate finance provided by public sources fell by two percentage points, to 44% of the total.

3.5.1 Multilateral channels for climate finance

Multilateral financial institutions and funds have multiple governing members, including both borrowing developing

countries and developed donor countries. These channels include multilateral (MDBs) and national development banks

(NDBs), the financial institutions that have been created within the framework of the United Nations Framework

Convention (UNFCCC) itself and United Nations (UN) agencies.

Multilateral development banks (MDBs) are broadly defined as development institutions with a banking business model.

In addition to their lending activities, they can also provide development research and advisory services. They play

a prominent role in delivering multilateral climate finance, with climate finance commitments of USD 43.1 billion

made in 2018 alone (EBRD et al., 2019). Many have incorporated climate change considerations into their core lending

and operations, and most MDBs now also administer climate finance initiatives with a regional or thematic scope.

The World Bank Group (WB) consists of the International Bank for Reconstruction and Development (IBRD) and the

International Development Association (IDA) and was founded in 1944. Originally aimed at supporting the reconstruction

of countries that were devastated in World War II, the focus shifted to supporting development in the Global South.

The World Bank’s carbon finance unit has established the Forest Carbon Partnership Facility (FCPF) to explore how carbon

market revenues could be harnessed to reduce emissions from deforestation and forest degradation, forest conservation,

sustainable forest management and the enhancement of forest carbon stocks (REDD+). It also manages the Partnership for

Market Readiness, aimed at helping developing countries establish market based mechanisms to respond to climate change

and the BioCarbon Fund, which is a public-private partnership that mobilizes finance for sequestration or conservation

of carbon in the land use sector.

The European Bank for Reconstruction and Development (EBRD) is a development bank, which has signaled explicitly that it focuses its

portfolio on the Green Economy Transition (GET) 2021-25 - the Bank’s new approach for helping countries where the EBRD works, to build

green, low carbon and resilient economies. Through the new GET approach, the EBRD will increase green financing to more than 50 percent

of its annual business volume by 2025. It also aims to reach net annual GHG emissions reductions of at least 25 million tons

over the

five-year period.

This ambition, announced at the latest annual meetings in London, October 2020 clearly shows that the EBRD is becoming

even more relevant lender for North Macedonian public and private sector.

EBRR has been very active in providing opportunities to private firms for climate finance. Currently an SMEs Competitiveness support scheme

is active for companies willing to invest in their competitiveness, including product and process improvements, procurement of equipment

and improving energy efficiency. For investments of up to EUR 1 million, the EBRD is offering a 15% grant upon successful performance.

This scheme emphasizes that

SMEs could use the loan for energy consumption and should use technologies that contribute to a green economy

by reducing pollutants such as greenhouse gas emissions.

Beyond this specific scheme, the EBRD can also directly lend to private sector

for investments over EUR 3 million.

National Development Banks (NDBs) are government-backed, sponsored, or supported financial institutions that have a specific

public policy mandate. NDBs come in many different shapes and sizes, and there is no one single or typical operating model.

NDBs can differ in terms of ownership structure, financial objectives, policy objectives (special purpose or multifunctional),

supervisory requirements, and financial instruments.

UNFCC Convention established a financial mechanism to provide financial resources to developing country Parties. The financial

mechanism also serves the Kyoto Protocol and the Paris Agreement. At COP 16, the Standing Committee on Finance was established

under the UNFCCC to assist the COP in meeting the objectives of the Financial Mechanism of the Convention. The Convention states

that the operation of the financial mechanism

can be entrusted to one

or more existing international entities

.

UNFCCC climate funds include the UN Adaptation Fund (AF), the Least Developed Country Fund (LDCF), the Special Climate

Change Fund (SCCF), and the Green Climate Fund (GCF).

The Global Environment Facility (GEF) established in 1991, is an operating entity of the financial mechanism of the UNFCCC,

serving in the same function for the Paris Agreement, with a long track record in environmental funding. GEF aims to help

developing countries and economies in transition contribute to the overall objective of the United Nations Framework Convention

on Climate Change (UNFCCC) to mitigate climate change, while enabling sustainable economic development. It also serves as

financial mechanism for several other conventions, including on biodiversity and desertification. Resources are allocated

targeting multiple focal areas, including climate change, according to the impact of dollars spent on environmental outcomes,

but ensuring all developing countries have a share of the funding. For the 7th replenishment period (2019-2022), close to 30

countries pledged USD 4.1 billion for all five focal areas, with an increase in funding for biodiversity and land degradation

neutrality, but a reduction in funding for climate change to USD 654 million, reflecting the growing role of the GCF. As of

December 2019, through the fourth, fifth, six and seventh Trust Fund, GEF had approved over 750 projects in the focal area of

climate change amounting to USD 2.8 billion.

The GEF also administers the Least Developed Countries Fund (LDCF)

and the Special Climate Change Fund (SCCF) under the guidance of the UNFCCC

Conference of Parties (COP). These funds support national adaptation plan development and implementation, although largely through smaller scale

projects (with a country ceiling for funding of USD 20 million). As of December 2019, the LDCF has made cash transfers to projects of USD 534

million and the SCCF has made cash transfers of USD 181 million, both since their inception in 2001 in close to 100 countries.

Formally linked to the UNFCCC, the Adaptation Fund (AF) is financed largely by government and private donors,

and also from a two percent levy on the sale of emission credits from the Clean Development Mechanism projects

under the Kyoto Protocol. Now mandated to serve the Paris Agreement, a similar automated funding source from a new carbon market

mechanism to be developed under the Paris Agreement is under consideration. However, in times of low carbon prices, the AF is

increasingly reliant on developed country grant contributions to stay afloat. Operational since 2009, total financial inputs

amount to USD 957 million, with total cash transfers to projects of USD 362 million. The AF pioneered direct access to climate

finance for developing countries through accredited National Implementing Entities that are able to meet agreed fiduciary as

well as environmental, social and gender standards, as opposed to working solely through UN agencies or Multilateral Development

Banks (MDBs) as multilateral implementing agencies. The sectors financed through the AF include agriculture, rural development,

water management, forestry, food security, disaster risk reduction, coastal risk reduction and urban development. The Fund also

provides readiness and capacity-building support through its Readiness Programme for Climate Finance, established in 2014.

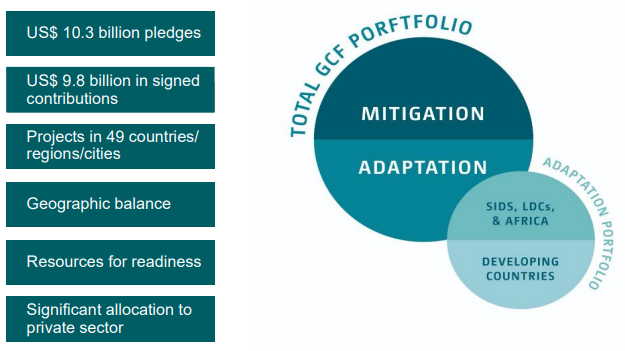

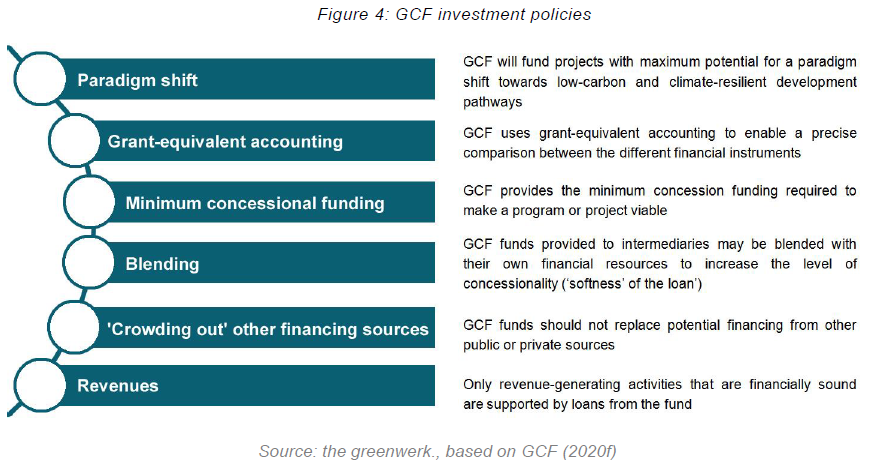

The Green Climate Fund (GCF) of the UNFCCC was agreed at the Durban COP and became fully operational with its first projects approved at the end of 2015.

Like the GEF, it serves as an operating entity of the financial mechanism of both, the UNFCCC and the Paris Agreement and receives guidance by the COP.

It is expected to become the primary channel through which international public climate finance will flow over time and is intended to fund the paradigm

shift toward climate-resilient and low-carbon development in developing countries with a country-driven approach, and a commitment to a 50:50 balanced

allocation of finance to adaptation and mitigation.

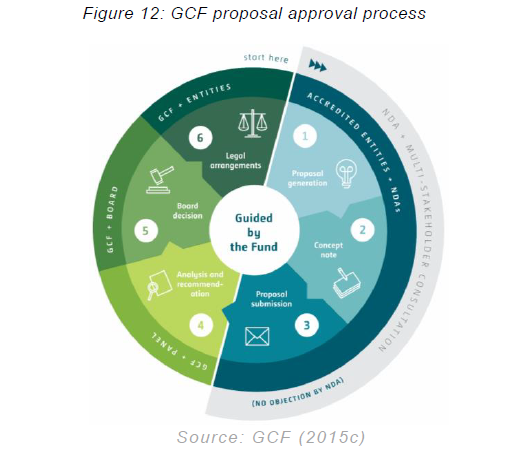

To receive money directly from the Green Climate Fund, entities need to be accredited as an “Accredited Entity” (AE). AEs can be international

(like the World Bank), regional (like the Secretariat of the Pacific Regional Environment Program or SPREP) or national (like a country’s environment ministry).

A list of currently accredited entities for the GCF can be found on the GCF’s website. Entities that prefer not to apply for accreditation have the option of

partnering with an institution that is already accredited. The Republic of North Macedonia accessed resources from the Green Climate Fund through the GCF Readiness

and Preparatory Support Programme. Two readiness projects have were approved with the Food and Agriculture Organization of the United Nations (FAO) serving as

the implementing partner, under the leadership and guidance of the

Cabinet of the Deputy President of the Government in charge of economic affairs, coordination

of economic departments and investments, as National Designated Authority for the GCF

. More information about the GCF Readiness and Preparatory Support Programme

implementation in North Macedonia can be found on the dedicated NDA webpage: www.greendevelopment.mk

Like MDBs, UN agencies commonly take on the role of administrator and/or intermediary of climate finance. The UN-REDD Programme

, made operational in 2008,

brings together UNDP, UNEP and FAO to support REDD+ activities, with the governance structure giving representatives of civil society and Indigenous People’s

organisations a formal voice.

Both MDBs and UN Agencies act as implementing entities for the GEF, SCCF, LDCF, AF and the GCF.

Export credit agencies (ECAs) provide funds (direct loans) or guarantees to facilitate exports. ECAs can remove the risk and uncertainty of payments to exporters

by shifting it to themselves in return for a premium. They can also underwrite the commercial and political risks of investments in overseas markets.

In recent years, the majority of medium and long term official export credit flows that go from OECD governments to developing countries have supported GHG

emitting sectors: transport (37%) and industry (26%), followed by energy projects (11%),

of which about 1% is estimated to go to renewable energy and energy

efficiency in the power sector

. Special liberalized rules governing the provision of ECA support for renewable energy and water projects were agreed by

several OECD countries, who are also engaged in negotiations to further strengthen the ability of export credit arrangements to support action against climate change.

3.5.2 Bilateral channels for climate finance

A significant share of public climate finance is spent bilaterally, administered largely through existing development agencies although a number

of countries have also set up special bilateral climate funds. However, there is limited transparency and consistency in reporting of bilateral

finance for climate change, with countries self-classifying and self-reporting climate-relevant financial flows without a common reporting

format or independent verification. The 2018 Biennial Assessment and Overview of Climate Finance Flows reported that USD 31.7 billion annually

in 2015-2016 was provided by developed to developing countries bilaterally,

in addition to that spent through climate funds and development

finance institutions

. An annual average of USD 30.3 billion in climate related ODA was reported to the Organization for Economic Cooperation

and Development – Development Assistance Committee (OECD DAC ) in the same year.

3.5.3 Regional and national channels and climate change funds

Several developing countries have established regional and national channels and funds with a variety of forms and functions, resourced through international

finance and/ or domestic budget allocations and the domestic private sector. The Indonesian Climate Change Trust Fund was one of the first of these

institutions to be established. Brazil’s Amazon Fund, administered by the Brazilian National Development Bank (BNDES), is the largest national climate

fund, with a commitment of more than USD 1.5 billion from Norway and Germany.

There are also national climate change funds in Bangladesh, Benin, Cambodia, Ethiopia, Guyana, the Maldives, Mali, Mexico, the Philippines, Rwanda, and South Africa.

Additional countries have proposed national climate funds in their climate change strategies and action plans. In many cases UNDP acted as the initial administrator of national funds,

increasing donor trust that good fiduciary standards will be met, but many countries are now passing these tasks on to national institutions.

National climate change funds attracted early interest, largely because they were established with independent governance structures that met high levels of

transparency and inclusiveness and could channel finance quickly to projects suited to national circumstances that were aligned with national priorities.

Working through coordinated national systems could also improve transaction efficiency.

At the same time, many developing countries are beginning to incorporate climate risk into their national fiscal frameworks, and monitoring climate related expenditure.

3.6 Private climate finance

A wide range of private sources can be tapped for the financing of private investment, as long as risk-return expectations are met.

These include the private companies themselves, local, regional and global commercial banks, non-bank financial institutions, leasing

companies, private equity investors and institutional investors (Climate Finance-Engaging the Private Sector-G20Report).

Private finance may be domestic or international. Some countries have mature capital markets, while others may not be able to provide private equity

or long tenor debt or even take the non-recourse project financing structures upon which much privately financed infrastructure depends. In mature markets,

international agencies can focus on addressing risk perception to catalyze private financing, while nascent markets may require a strengthening of the local

financial sector and capacity building in order to do so.

Private climate finance reached a record high of USD 330 billion in 2017, representing an increase of USD 99 billion from 2016, or 43% year-on-year growth.

However, financing fell slightly in 2018 to USD 323 billion, in response to macroeconomic trends resulting in a dampened global investment environment,

as well as continued decreases in global renewable energy capital costs.

Commercial financial institutions are entities such as banks and other financial institution that provide financial services

to non-financial institutions, households and governments. They also invest in physical facilities, such as buildings, using

funds raised domestically or from foreign sources. They are responsible for one to seven percent of the investment in new physical assets.

Private equity capital usually involves later stages of investment and is often sourced from pooled funds.

The key actors are private equity firms, which can range from very small to very large (both with respect to the number of

people involved and the assets under management). Since these investments tend to be made at a more mature stage in a project

or company development, they involve lower risks and the expected return is also likely to be lower than that of angel investors

or venture capitalists. Nevertheless, the risk-return profile associated with private equity is still likely to be higher than

that associated with public equity finance. Forms of private equity finance include:

o Angel capital

Angel capital is private equity finance provided to companies,

technologies, or projects that are particularly small, new, and hence, risky. Such early stage investments are usually very high

risk and experience high failure rates. However, if they succeed, they expect very high returns. The key actors tend to be wealthy

individuals, whose investment are sometimes facilitated by family offices or groups of individuals)

o Venture capital

Venture capital is another form of private equity finance for early-stage investment,

although it is usually in a more organised form than angel capital. The key actors tend to be groups of wealthy individuals and specialized

teams of venture capitalists who target returns that are multiples of their original investment. The high returns are seen as compensation

for the high risk of investing at an early stage.

o Corporations

Business can finance climate investment projects by using either on-balance sheet financing

or borrowing funds from a bank in the form of a loan, or through equity capital from selling a stake in the business itself. The borrowing

capacity of power utilities is large. With a current market capitalization of the global electricity market estimated at USD 1.5 to USD 2

trillion, power utilities could potentially raise USD 3 trillion to USD 6 trillion in debt to fund clean energy projects.

Given their pivotal importance for green investment, institutional investors have a long-term investment horizon, which matches the

long-term financing requirements of climate investment such as wind power or timber forestry. The term ‘institutional investors’ may be described